Homeowners insurance is an essential part of protecting your home and belongings. It provides financial coverage in case of unexpected events like fire, theft, or natural disasters. However, not everyone qualifies for homeowners insurance. Some factors can make you ineligible for coverage, leaving you in a challenging situation. Understanding these factors can help you take the necessary steps to secure an insurance policy.

Why Homeowners Insurance Matters

Homeowners insurance is not just a recommendation; for many, it’s a requirement. Mortgage lenders often mandate it to protect their investment in your home. Even if you own your home outright, having homeowners insurance safeguards you from major financial losses. It covers damage to your home, personal property, and even liability if someone gets injured on your property.

However, not every home or homeowner qualifies for coverage. If you’ve been denied homeowners insurance, it’s important to understand why. Below are some common reasons that can make you ineligible for homeowners insurance.

Factors That Can Disqualify You from Homeowners Insurance

1. Poor Insurance Score

Your insurance score, similar to a credit score, is based on your financial history and past insurance claims. Insurance companies use this score to assess your risk level. If you have a low insurance score due to missed payments, high debt, or previous claims, you may be denied coverage or face high premium rates.

2. Criminal Convictions

If you have a history of criminal activity, especially offenses related to property damage, fraud, or arson, insurance companies may see you as a high-risk client. Even if your criminal record is unrelated to homeownership, insurers may still hesitate to provide coverage.

3. Lapsed Insurance Coverage

A history of not maintaining continuous insurance coverage can raise red flags. If you previously had homeowners insurance but allowed it to lapse due to non-payment or other reasons, insurance companies may view you as unreliable and deny you a policy.

4. Frequent Claims History

If you or previous homeowners have made multiple insurance claims, insurers may consider the property high-risk. Claims related to fire damage, liability lawsuits, or theft can particularly impact your eligibility. Even if the claims were not your fault, the history alone can lead to coverage denial.

5. High-Risk Home Location

The location of your home plays a significant role in determining your eligibility for insurance. If your home is in a high-crime neighborhood, insurers may be concerned about frequent theft or vandalism. Similarly, homes in flood zones, wildfire-prone areas, or far from fire stations may be ineligible for standard homeowners insurance.

6. Hazardous Home Features

Certain features on your property can increase liability risks, making it harder to get insurance. Common hazardous features include:

- Swimming pools – Pools pose drowning risks and potential liability claims.

- Trampolines – Trampoline injuries are common, leading to lawsuits.

- Treehouses – These can be dangerous, especially for children.

- Wood-burning stoves – These increase the risk of house fires.

- Outdated electrical systems – Faulty wiring can lead to fire hazards.

If your home has these features, you may need additional liability coverage or risk being denied insurance altogether.

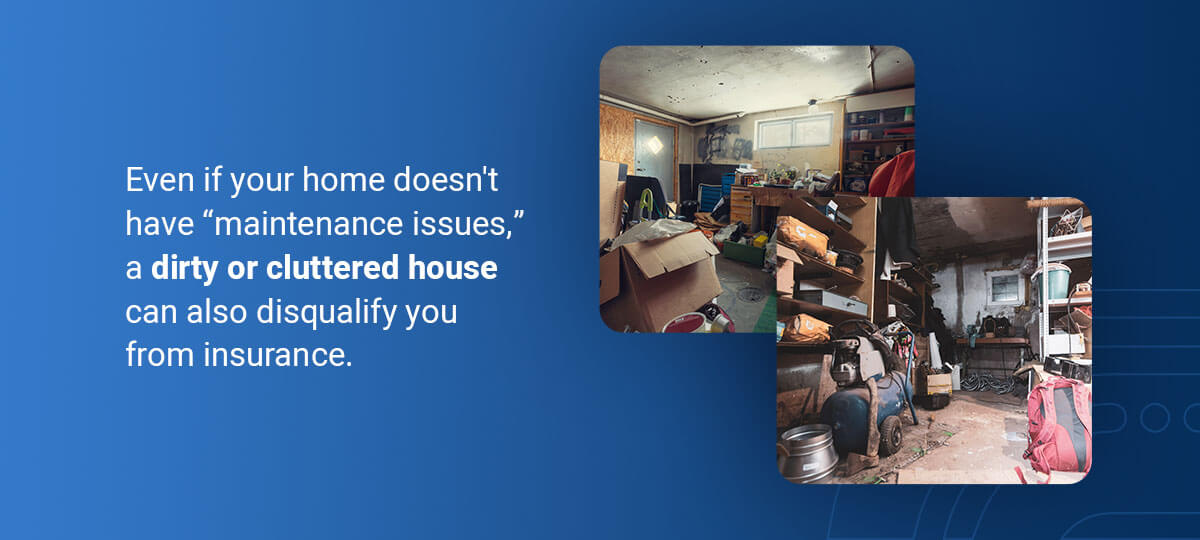

7. Poor Home Maintenance

Insurance providers may deny coverage if your home is in poor condition. A home inspection often determines whether your home is well-maintained. Issues that could make you ineligible include:

- A leaking roof – Water damage from a neglected roof can lead to costly repairs.

- Cracked foundation – Structural problems make a home unsafe.

- Outdated plumbing or electrical systems – These increase the risk of fires and water damage.

- Mold infestations – Mold can cause health problems and extensive damage.

If your home has significant maintenance issues, insurers may refuse coverage until repairs are made.

8. Part-Time Vacancy

If your home is vacant for extended periods, insurance companies may see it as a higher risk. An unoccupied home is more vulnerable to damage from break-ins, vandalism, and unnoticed leaks or fires. If you plan to leave your home vacant for months at a time, you may need a special vacant home insurance policy.

9. Running a Business from Home

If you operate a business from your home, your homeowners insurance may not cover certain liabilities. Businesses that involve customers visiting your home, storing inventory, or using specialized equipment might require business insurance instead. If an insurer determines that your home is also a business location, they could deny you homeowners coverage.

What to Do If You Can’t Get Homeowners Insurance

If you’ve been denied homeowners insurance, don’t panic. There are steps you can take to improve your chances of securing coverage:

- Improve Your Insurance Score – Pay off debts, avoid late payments, and maintain good financial habits to boost your score.

- Fix Home Maintenance Issues – Address problems like roof leaks, electrical hazards, and plumbing issues to make your home insurable.

- Consider High-Risk Insurance – Some states offer high-risk insurance programs for homeowners who can’t get standard policies.

- Remove Hazardous Home Features – If possible, get rid of trampolines, repair structural issues, or install safety features to reduce risk.

- Shop Around for Other Insurers – Different companies have different criteria, so check multiple providers to find one that will cover your home.

Is It Illegal to Not Have Homeowners Insurance?

Unlike car insurance, homeowners insurance is not legally required. However, if you have a mortgage, your lender will likely require it. If you don’t maintain coverage, your lender may purchase insurance on your behalf at a much higher cost. Even if you own your home outright, skipping insurance leaves you financially vulnerable in case of unexpected damage or liability claims.

Final Thoughts

Homeowners insurance provides essential protection for your home, but not everyone qualifies. Factors like poor credit, past claims, home hazards, and high-risk locations can make you ineligible. If you’re struggling to get coverage, take steps to improve your eligibility by fixing home maintenance issues, improving your credit score, and shopping around for the right insurer.

Understanding what makes you ineligible for homeowners insurance helps you prepare and take proactive steps to secure the protection you need. If you’re currently facing challenges in obtaining coverage, start addressing the risk factors today to improve your chances of getting insured.